Tech Weekly: Stock Valuation Fears Persist as US Government Reopens

We also break down next week’s catalysts to watch to help you prepare for the week ahead.

In this article:

This week’s tech sector performance

This past week highlighted the balancing act between fiscal policy progress, macroeconomic uncertainties and sector-specific pressures, setting the stage for cautious navigation as markets brace for more data and policy signals ahead.

Market action started with notable optimism as US futures jumped on Monday (November 10) in anticipation of the Senate’s passage of a new spending bill, ending the government shutdown and reopening the door for delayed economic data releases. The relief rally saw major indexes close higher; however, Tuesday’s (November 11) weaker-than-expected ADP employment report reignited concerns over labor market softness.

Wednesday (November 12) brought further clarity as the House approved the spending legislation, solidifying government funding. This helped global markets rally, though comments from Federal Reserve officials underscored ongoing vigilance against inflation, tempering exuberance and keeping gains in check.

Meanwhile, news of SoftBank’s (OTC Pink:SOBKY) sizable sale of its NVIDIA (NASDAQ:NVDA) holdings and Michael Burry’s US$1.1 billion “big short” bet against artificial intelligence (AI) stocks via put options on NVIDIA and Palantir Technologies (NASDAQ:PLTR) added pressure on AI-driven tech stocks.

Mixed earnings reports midweek also set the tone for an uneven performance in the tech sector.

CoreWeave (NASDAQ:CRWV) and Applied Materials (NASDAQ:AMAT) both reported disappointing results relative to expectations, with CoreWeave’s revenue guidance trimmed due to data center delays and Applied Materials seeing year-over-year revenue declines despite an earnings beat.

Despite posting record revenues fueled by AI chip demand, Taiwan Semiconductor Manufacturing Company (NYSE:TSM) saw some profit taking amid cautious outlook commentary. Analysts also noted that the company’s revenue growth rate slowed in Q3 compared to previous quarters, tempering enthusiasm.

Conversely, Advanced Micro Devices (AMD) (NASDAQ:AMD) delivered a strong beat with robust revenue and earnings, which was met with enthusiasm from investors in extended trading on Tuesday and into Wednesday’s open.

On Thursday (November 13), Canada unveiled its next tranche of major infrastructure projects, signaling long-term investment potential, but the market reaction was mixed amid incomplete detail and broader investor caution.

Futures dipped ahead of the session, and a pronounced selloff in big tech names weighed heavily on equity benchmarks, which led to a premarket decline on Friday (November 14).

However, early losses gave way to a rebound, led by strong gains in NVIDIA shares. Investors viewed the dip as a buying opportunity for expensive names, despite earlier concerns over stretched AI stock valuations. NVIDIA, which initially fell 3.4 percent, surged back in afternoon trading, pulling the broader market upward.

3 tech stocks moving markets this week

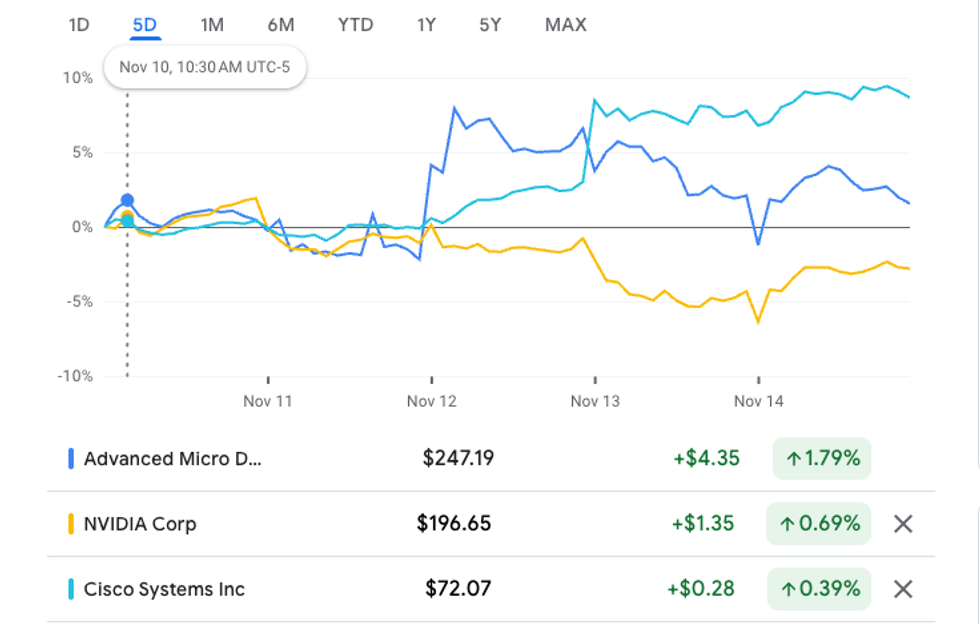

1. Advanced Micro Devices (NASDAQ:AMD)

AMD reported strong quarterly results on Tuesday, exceeding revenue and earnings expectations driven by robust demand for its next-generation chips across data centers and gaming segments.

Revenue rose 12 percent year-over-year, supported by growth in AI-related processors and expansion into new enterprise markets. AMD also raised its full-year guidance, signaling confidence in sustained momentum amid increased adoption of AI and advanced computing technologies.

The market reacted positively, with AMD shares pushing the Nasdaq higher on Wednesday morning. Its share price climbed over 2.40 this week to close at US$247.96.

2. Cisco Systems (NASDAQ:CSCO)

Cisco also reported a strong earnings beat, with revenue rising 8 percent year-over-year to US$14.9 billion and non-GAAP EPS increasing 10 percent to US$1.00 for the first-quarter fiscal 2026 period, surpassing analyst expectations.

The company cited robust demand for AI-related networking products and a multi-year campus refresh opportunity, which led it to raise its full-year revenue forecast above prior estimates.

This positive outlook and solid performance drove Cisco shares to a 25-year high, with the stock outperforming the broader tech sector on Thursday, signaling investor confidence in the company’s growth trajectory amid accelerating AI adoption. Its share price closed 8.7 percent higher at US$78 on Friday.

3. NVIDIA (NASDAQ:NVDA)

NVIDIA staged an impressive comeback on Friday after starting the day with a steep loss.

The stock bounced from a low near US$180.58 to a high of US$191.01, driven by renewed investor optimism amid projected ongoing demand for its AI and data center chips.

Despite recent volatility and market concerns about stretched AI valuations, NVIDIA’s critical role in the AI revolution and anticipation of strong upcoming earnings helped fuel buying momentum. It closed at US$190.17, a 2.54 percent decrease for the week but an improvement from an earlier decline.

AMD, NVIDIA and Cisco Systems performance, November 10 to 14, 2025.

Chart via Google Finance.

Top tech news of the week

- Cleo, a Canadian legal software provider, has secured C$500 million in a funding round led by New Enterprise Associates and included other existing investors. The new funds elevate its valuation from C$3 billion to C$5 billion, making it one of Canada’s most valuable tech startups.

Tech ETF performance

Tech exchange-traded funds (ETFs) track baskets of major tech stocks, meaning their performance helps investors gauge the overall performance of the niches they cover.

This week, the iShares Semiconductor ETF (NASDAQ:SOXX) declined by 4.62 percent, while the Invesco PHLX Semiconductor ETF (NASDAQ:SOXQ) saw a weekly loss of 4.73 percent.

The VanEck Semiconductor ETF (NASDAQ:SMH) decreased by 3.55 percent.

Tech news to watch next week

Next week, investors will be scrutinizing earnings reports from Palo Alto Networks (NASDAQ:PANW) and AI bellwether NVIDIA on November 19, with analysts projecting revenue of US$2.46 billion and US$54.9 billion, respectively.

Also, traders may finally begin receiving some important economic data releases after a recent lull, though some readings could still be delayed as statistical agencies update their schedules and catch up following recent disruptions.

The US ADP unemployment report for November, due on November 18, will shed some light on the state of the job market ahead of the release of Federal Reserve minutes from its October meeting on November 19.

November 20 could bring the first initial jobless claim in over five weeks, while this week’s release of the consumer sentiment survey from the University of Michigan will reveal updated consumer confidence levels.

Securities Disclosure: I, Meagen Seatter, hold no direct investment interest in any company mentioned in this article.